Recommandé

Contenu connexe

Tendances

Tendances (18)

En vedette

En vedette (20)

Similaire à Modelos economicos

Similaire à Modelos economicos (20)

Plus de Francoveliz

Dernier

Dernier (20)

Modelos economicos

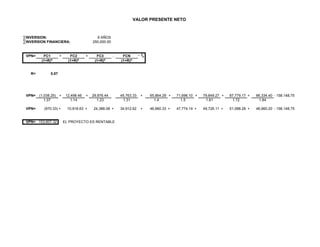

- 1. VALOR PRESENTE NETO ∑INVERSION: 9 AÑOS ∑INVERSION FINANCIERA: 250,000.00 VPN= FC1 + FC2 + FC3 … FCN - IO (1+R)N (1+R)N (1+R)N (1+R)N R= 0.07 VPN= (1,038.25) + 12,498.46 + 29,876.44 45,763.33 + 65,864.29 + 71,696.10 + 79,849.27 + 87,779.17 + 86,334.40 - 158.148,75 1.07 1.14 1.23 1.31 1.4 1.5 1.61 1.72 1.84 VPN= (970.33) + 10,916.63 + 24,388.08 + 34,912.62 + 46,960.33 + 47,774.14 + 49,726.11 + 51,088.28 + 46,960.20 - 158.148,75 VPN= 153,607.32 EL PROYECTO ES RENTABLE

- 2. POLICÍA MUNICIPAL MUNICIPIO JUAN JOSÉ MORA FLUJO DE EFECTIVO PERIODOS 2010 2011 2012 2013 2014 2015 2016 2017 2018 UTILIDAD NETA -10,509.25 12,028.46 30,158.44 46,827.33 69,913.29 77,620.10 86,707.27 95,773.17 94,865.40 DEPRECIACION 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 SUB-TOTAL MAS: LIMITACION CTAS. POR COBRAR AUMENTO CTAS. POR COBRAR MENOS: AUMENTO CTAS. POR COBRAR DISMINUCION CTAS. POR PAGAR EFECTIVO NETO USADO -1,038.25 21,499.46 39,629.44 56,298.33 79,384.29 87,091.10 96,178.27 105,244.17 104,336.40 ACTIVIDADES DE INVERSION MAS: DISMINUCUION DE PROPIEDADES Y EQUIPOS MENOS: AUMENTO DE PROPIEDADES Y EQUIPOS 9,001.00 9,753.00 10,535.00 13,520.00 15,395.00 16,329.00 17,465.00 18,002.00 EFECTIVO NETO USADO (9,001.00) (9,753.00) (10,535.00) (13,520.00) (15,395.00) (16,329.00) (17,465.00) (18,002.00) ACTIVIDADES DE FIANCIAMIENTO MAS: AUMENTO DE FINANCIAMIENTO - 9,001.00 9,753.00 10,535.00 13,520.00 15,395.00 16,329.00 17,465.00 18,002.00 MENOS: DISMINUCION DE FINANCIAMIENTO EFECTIVO NETO PROVISTO DE FINANCIAMIENTO 9,001.00 9,753.00 10,535.00 13,520.00 15,395.00 16,329.00 17,465.00 18,002.00 TOTAL FLUJO DE CAJA (1,038.25) 12,498.46 29,876.44 45,763.33 65,864.29 71,696.10 79,849.27 87,779.17 86,334.40

- 3. ESTADO DE RESULTADO PROYECTADO EMPRESA HELADERIA INDUSTRIAL DE PUERTO CABELLO, S.A. DEL 2003 AL 2011 INGRESOS POR SERVICIO 2010 2011 2012 2013 2014 2015 2016 2017 2018 INGRESOS NETOS 40,000.00 65,000.00 84,000.00 102,000.00 126,000.00 140,233.01 150,383.01 160,533.01 170,683.01 COSTOS Y GASTOS INSUMOS 79.75 84.54 86.23 88.81 90.59 103.27 105.34 107.44 128.93 GASTOS DE ENERGIA ELECTRICA 960.00 1,017.60 1,037.95 1,069.09 1,090.47 1,243.14 1,268.00 1,293.36 1,552.03 PERSONAL 30,000.00 31,800.00 32,436.00 33,409.08 34,077.26 38,848.08 39,625.04 40,417.54 48,501.05 DEPRECIACION VEHÍCULOS 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 9,471.00 COSTOS VARIABLES ALQUILER DEL LOCAL 720.00 763.20 778.46 801.82 817.85 932.35 951.00 970.02 1,164.03 MANTENIMIENTO DE EQUIPO 1,578.50 1,673.21 1,706.67 1,757.87 1,793.03 2,044.06 2,084.94 2,126.64 2,551.96 GASTOS (FINANCIAMIENTO) 7,700.00 8,162.00 8,325.24 8,575.00 8,746.50 9,971.01 10,170.43 10,373.84 12,448.60 IMPUESTO MUNICIPALES UTILIDAD NETA ANTES DEL I.S.R.L. (10,509.25) 12,028.46 30,158.44 46,827.33 69,913.29 77,620.10 86,707.27 95,773.17 94,865.40 I.S.R.L. UTILIDAD NETA -10,509.25 12,028.46 30,158.44 46,827.33 69,913.29 77,620.10 86,707.27 95,773.17 94,865.40

- 4. Modelo Económico Presupuesto de Inversión Monto a Financiar Descripción 2010 Aportes Propios Total Bs. Insumos 79,750.00 0 79,750.00 Maquinarias y Equipos - 0.00 Equipos de Seguridad 137,500.00 0 137,500.00 Vehículos 38,500,000.00 38,500,000.00 Equipos de Comput. 30,000.00 30,000.00 Uniformes del Personal 10,000.00 10,000.00 Mobiliario y Equipos 82,500.00 82,500.00 38,839,750.00 COSTO DE MANTENIMIENTO DE EQUIPOS 38,667,500.00 ESTIMADO 1% 1er AÑO 386,675.00 GASTOS ENERGIA ELECTRICA 12,000.00 50 PERSONAS S/MINIMO 75,000.00 ALQUILER DEL LOCAL 6,000.00 FINANCIAMIENTO - ESTIMADO 7% 1er AÑO - DEPRECIACIÓN 15 AÑOS 2,320,050.00 38,839,750.00 100.00% APORTE FINANCIADO 38,839,750.00 INGRESOS POR Años PRESTACIÓN SERVICIO P/U SERVICIO 2010 10,000.00 14.02 140,233.01 2011 10,500.00 14.32 150,383.01 2012 11,000.00 14.59 160,533.01 2013 11,500.00 14.84 170,683.01

- 5. CALCULO DEL COEFICIENTE DE VARIANZA ESTANDAR Y= Ingresos por Servicio Prestado 8 X= Cantidades de unidades promedio 20% Operativas 80% Recaudación ∑X2 = 269,500,000.00 S2 = 19,954,574,433.66 N= 5.00 X= 36,000.00 ∑X2 S2 1 S2 Sb1= * Sb2= * N*∑X *(X) 2 2 ∑X - 1 (X) 2 2 N 269,500,000.00 19.954.574.433,66 1 19.954.574.433,66 Sb1= * Sb2= * 5 * 269.500.000,00 * (36.000,00)2 269.500.000,00 - 1 * (36.000,00) 2 5 269,500,000.00 19.954.574.433,66 1 19.954.574.433,66 Sb1= * Sb2= * 1.347.500.000,00 * 1.296.000.000,00 269.500.000,00 - 1 * (36.000,00) 2 5 269,500,000.00 19.954.574.433,66 1 19.954.574.433,66 Sb1= * Sb2= * 1,746,360,000,000,000,000.00 269.500.000,00 - 1 * 1.296.000.000,00 5 Sb1= 0.000000000154 19.954.574.433,66 1 19.954.574.433,66 * Sb2= * 269.500.000,00 - 259.200.000,00 Sb1= 3.07 1 19.954.574.433,66 Sb2= * 10,300,000.00 Sb1= 0.000000097087 * 19.954.574.433,66 Sb1= 1,937.33

- 6. CALCULO DEL ERROR ESTANDAR DE ESTIMACIÓN Y= Ingresos por Prestación del Servicio 8 X= Cantidades de unidades promedio 20% Operativas 80% Recaudación Año X Y XY X² y² 2003 5000 40,000.00 200,000,000.00 25,000,000.00 1,600,000,000.00 2004 6500 65,000.00 422,500,000.00 42,250,000.00 4,225,000,000.00 2005 7000 84,000.00 588,000,000.00 49,000,000.00 7,056,000,000.00 2006 8500 102,000.00 867,000,000.00 72,250,000.00 10,404,000,000.00 2007 9000 126,000.00 1,134,000,000.00 81,000,000.00 15,876,000,000.00 Σ 36000 417,000.00 3,211,500,000.00 269,500,000.00 39,161,000,000.00 B2 = 20.30 B1 = -62,766.99 Y= 83,400.00 X= 7,200.00 ∑ e 12 S2 = N -2 e12 = ∑ Y2 - B1∑ Y- B2 ∑ (XY) 26,173,834,951.46 -5,471,111,650.49 e12 = 39.161.000.000,00 - (-62.766,99)(417.000,00) - 20,30(269.500.000,00) e 12 = 39,161,000,000.00 + 26.173.834.951,46 - 5.471.111.650,49 e 12 = 59,863,723,300.97 S2 = 59,863,723,300.97 3.00 S2 = 19,954,574,433.66 S= 141,260.66

- 7. MODELO ECONÒMICO FORMULAS BASICAS Ŷ = B1 ± B2 + U __ B1 = Ŷ - B2 (X) B2 = N Σ (XY) - Σ X . ΣY N Σ X² - Σ (X)² DETERMINACION DE VARIABLES Y= Ingresos por prestación del servicio 8 X= Cantidades de unidades promedio 20% servicio 80% recaudación Año X Y XY X² 2010 5000 40,000.00 200,000,000.00 25,000,000.00 2011 6500 65,000.00 422,500,000.00 42,250,000.00 2012 7000 84,000.00 588,000,000.00 49,000,000.00 2013 8500 102,000.00 867,000,000.00 72,250,000.00 2014 9000 126,000.00 1,134,000,000.00 81,000,000.00 Σ 36000 417,000.00 3,211,500,000.00 269,500,000.00 B2 = N ∑ (XY) - ∑ X . ∑Y N ∑ X2 - ∑ (X) 2 B2 = 5 (3.211500.000,00) - (36.000,00 x 417.000,00) 5 (269.500.000,00) - (36.000,00)2 B2 = 16,057,500,000.00 - 15,012,000,000.00 1,347,500,000.00 1,296,000,000.00 B2 = 1,045,500,000.00 51,500,000.00 B2 = 20.30 20.30097087 Y= ∑Y

- 8. N Y= 417,000.00 5 Y= 83,400.00 X= ∑X N X= 36,000.00 5 X= 7,200.00 B1 = Y - B2. (X) B1 = 83,400.00 - 20.30 7,200.00 B1 = 83,400.00 - 146,166.99 B1 = -62,766.99 Ŷ= B1 ⁺ B2 X + μ Ŷ= -62,766.99 + 20.30097087 X +μ

- 9. Proyección Ŷ= -62,766.99 + 20.30 X +μ Año X Y 2010 10,000.00 140,233.01 Ŷ año 2008 = -62,766.99 + 20.30 10,000.00 2011 10,500.00 150,383.01 2012 11,000.00 160,533.01 Ŷ año 2008 = -62,766.99 + 203,000.00 2013 11,500.00 170,683.01 Total 43,000.00 621,832.04 Ŷ año 2008 = 140,233.01 Ŷ año 2009 = -62,766.99 + 20.30 10,500.00 Ŷ año 2009 = -62,766.99 + 213,150.00 Ŷ año 2009 = 150,383.01 Ŷ año 2010 = -62,766.99 + 20.30 11,000.00 Ŷ año 2010 = -62,766.99 + 223,300.00 Ŷ año 2010 = 160,533.01

- 10. Ŷ año 2011 = -62,766.99 + 20.30 11,500.00 Ŷ año 2011 = -62,766.99 + 233,450.00 Ŷ año 2011 = 170,683.01