How to Sell Bank Loans

•

63 j'aime•36,347 vues

This powerpoint was created to teach commercial lenders how to sell their bank as a more expensive (but more valuable) alternative to regular banks. The slides themsevles were kept clean - the "meat" is in the speaker's notes.

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (19)

Similaire à How to Sell Bank Loans

Similaire à How to Sell Bank Loans (14)

Dernier

Dernier (20)

How to Sell Bank Loans

- 4. No longer the lender of last resort.

- 5. 1. The stuff that makes us different.

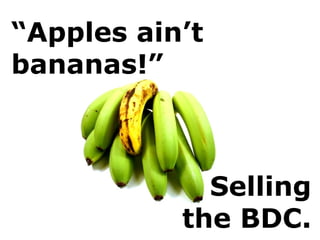

- 6. They sell good ol’ bananas…

- 7. …while we sell juiced- up apples.

- 10. the relationship over any one transaction. We value

- 13. Security is up. not our big hang-

- 14. We don’t have a short fuse.

- 17. We are amazed by our clients.

- 19. We ask a lot of good questions...

- 20. We are, after all, a development bank.

- 22. We are not a pain to deal with.

- 24. regular bank not aWe are

- 27. We’ll break bread with you (and pick-up the tab).

- 29. We can be pretty creative.

- 31. 93% > 58%

- 32. We are a great alternative.

- 34. Go face-to-face.

- 36. While we don’t compete on rate… %

- 37. …they need to feel you sharpened your pencil.

- 39. DEMO: Interest Rate Comparative Model “A straight beats a blend…”

- 42. “I don’t give my bank a personal guarantee!”

- 43. “Why should I pay a study fee?”

- 44. “Why should I provide Review statements?”

Notes de l'éditeur

- POSITION THE BANK FIRST. This workshop is about how to sell the Bank as a whole to an influencer or prospect – as opposed to negotiating a particular loan or CG transaction.

- WHY SHOULD I DEAL WITH YOU? By law, BDC exists to complement the offerings of the other banks. And yet you will be asked countless times, “So what makes you guys different from the other banks? Why should my clients deal with you? Why should I refer a client to you if they’re already dealing now with TD Bank?” BE READY TO ANSWER. And you do have to be ready for those questions. Practise your answers. That’s what this workshop is about. Get a copy of it and read the speaker’s notes too.

- COMPLEMENTARY LENDER DEFINED. We exist to add-to or top-up the financing they are getting from their day-to-day banker. We don’t want to replace their regular bank. We’ll talk today about emphasizing point of difference when faced with a so-called ‘competing’ term sheet but complementing comes a lot of ways: Preserving W/C. When we do a leveraged loan for say equipment, not only do they have extra capacity to grow sales but they have the W/C to do it. This makes them a better credit risk for the other bank. If the other bank has portfolio balancing concerns and must say ‘no’ to a transaction we can step in and do the deal which prevents that client from ‘firing’ CIBC and wandering down the street to RBC. Often when we scrub down a deal we notice that the CB could be playing a greater role. SO we do a loan with a c.c. for an increased operating line of credit. When we pump $250K of sub-debt into a company subordniated to the CB we just improved their risk position. GAP FILLER. We should focus primarily on loans that other Banks don’t have the risk appetite to do. Our whole mandate is written (see Corporate Plan Summary) with the words ‘gap filler’ peppered throughout the text. COMPANIES GROW IN STEPS AND PLATEAUS [FLIPCHART]. There’s no such thing as a smooth growth curve. Every time there’s a development project that’s where we come in. The rest of the time the daily banking stuff is best left to their regular bank. NOT ABOUT THE TRANSACTION ANYWAY. Besides if we are competing for anything it’s the business, not the individual transaction. If the other bank offers a better deal, we’ll advise the client to take it.

- ARE YOU STILL HEARING THIS? We turned over a new leaf ages ago! Don’t let these words be uttered from your lips. Depending on your market you may not hear this one anymore. LENDER of LAST RESORT. “We sold the last resort years ago – ha!” A little humour goes a long way. Actually though, explain that our mandate changed officially in 1995 and had ceased to be a practical reality years before that. Explain our mandate to complement our friends at the regular banks in order to develop SMEs.

- CONFUSING. We don’t ‘compete’ we ‘complement’ yet when we are face-to-face with a customer they certainly hope we can give them a good deal. And your managers and VPAMs will also ask you to ‘fight’ for our deals. OK TO EMPHASIZE OUR POINTS OF DIFFERENCE. We want you to diagnose the client’s problem and present a solution. Our solutions are often remarkably different than other banks’ and it’s our job as salespeople to showcase those differences. That’s not really competing head-to-head on interest rate though. DON’T KICK A SLEEPING DOG. If you truly are comparing a banana to a banana and it’s just coming down to interest rate then let ‘em go. If we do go head-to-head one too many times with the other bank we’re going to get challenged at the Minister’s level by the other banks (this has happened in the past). BACK IN THE BRANCH. When you get home you’ll hear a lot of “yeah, but…” language where fellow AMs tell you to compete head-on. Resist the urge. Learn how to sell properly. Apples aren’t bananas. The Scotia Bank in Richmond Hill won’t let us in the building and in Quebec, TD staff are not allowed to make us a referral “on pain of death.” WE DO 7,800 LOANS A YEAR. If you sell the Bank properly (i.e., emphasize points of difference), you will certainly hear the interest rate objection far less. Obviously it works as we do a lot of loans every year. You won’t win them all but there are 987,500 fish in the sea (and we’ve only talked to 24,500 so far).

- BANANAS ARE GOOD FOR YOU. There’s nothing wrong with a banana. To grow everyone needs a solid chartered bank relationship. Don’t put the banks down. Compliment them and Complement them. SEGUE. We’re a gap filler, not a substitute….

- …SO WE PICK UP WHERE THEY LEAVE OFF…rather than be a substitute for them. IF WE WERE THE SAME, THERE’D BE NO NEED FOR BDC. A big point of difference between BDC and regular banks is that our loans are not the same as their loans. We have completely different appetites for risk. COURTESY CALL. If the other Bank, however, feels we compete with them it could hurt us later. So in cases of head-to-head term sheets – have your Branch Manager or VPAM talk to the other bank and confirm in advance they don’t mind us doing our deal. Invite them to match our terms. No need to do this in many cases as the CB’s are often unaware the client even wanted some help in the first place (thus no competition on the deal per se)

- #1 DIFFERENCE = PROFIT MOTIVATION. This ain’t us. We’re about growing companies, not maximizing our own profits.

- OVERLY DEAL-FOCUSED. Some financial institutions seem more interested in closing the deal to add another income generating asset to the portfolio. If it looks like a ‘go’ they pay attention to you, otherwise they drop you fast.

- GOLDEN GOOSE EGG. By contrast, we’re not after market share, we’re after share of wallet. We value not just any one single transaction but rather a never ending stream of referrals and transactions. PROFIT MOTIVATION. We are profitable enough to be self-sustaining and to grow our equity base to support even more SMEs in the future. We are not, however, trying to maximize profitability. This is in sharp contrast to Chartered Banks who have hungry shareholders clamoring for dividends and rising share prices. Therefore, we don’t have to charge our clients fees every time they pick up the phone and call us.

- WE OFFER DIVERSIFICATION. Our biggest point of differentiation. In the same way that we tell our customers that they should not be relying on 1 or 2 customers nor should they rely on one bank.

- CAN YOU IMAGINE A TIME IN THE NEXT 15 YEARS…? We never know what the future holds. If you hit a rough patch 9 years from now, will your banker support you if they are the only ones calling the shots? SHORT VERSUS LONG TERM DEBT. Why not put all your long term financing with a long term partner like the BDC and all your short term financing with your day-to-day bank who loves short term financing. This will ensure you have a plant to operate from and you will always be able to get an operating line of credit if you have good receivables.

- SECURITY IS NOT KING (Cashflow is!): The perception out there is that it is like pulling teeth to get anything out of a Banker and that you must pledge a $1 to get a $1 as well as pledge your first born. Almost every other commercial lender’s #1 credit criteria is collateral. For us, collateral is less important. 95% of our portfolio is ‘under water.’ GE CAPITAL. We once had an AM that used to work there. He found BDC ‘liberating’ because back at GE he had to show a security coverage matrix for each year of a 4 year lease demonstrating how the RLV exceeded the T/C at all points. At no point could they be undersecured.

- THUS, A RELATIVELY FRIENDLY WORKOUT GROUP: Fully 17% of SAD deals are returned to the branch as performing accounts (compare to 0.5% at typical Chartered Bank) Because we are under-secured on 95% of our portfolio, it is in our own best interest to help companies return to viability, rather than automatically selling off their assets. Don’t get me wrong – SAD is serious about resolving our unpaid loans and can play hard ball as well as the best of them if they are forced to. However, they approach every client with respect and prefer to upgrade an account rather than liquidate it. If the “corpse has a pulse” they’ll try to save it. If the business is clearly not viable they will liquidate. DON’T EVER SAY WE WON’T PURSUE PERSONAL GUARANTEES (it simply is not true)

- WE ARE DECISIVE. You can count on us for a quick yes or no. No long drawn out maybes. Particularly useful differentiating factor when talking to influencers. Get good at the professional, gentle (but quick) decline. They’ll respect your decision-making, if not the decision!

- ON MERIT. We judge every loan as a unique case, we don’t have a lending template or hard-wired criteria that must be surpassed to get an approval. CREDIT SCORED. For smaller loans in particular, several of the other Banks have a giant face-less underwriting centre where deals get processed. The deals need to fit squarely in the right hole or they get rejected. By contrast, we have a human making every decision. We will never be Wells Fargo.

- WHY YOU JOINED THE BDC. If you came to BDC because you get a charge out of working directly with SMEs where you get to negotiate directly with the most senior decision maker, get an entrepreneurial kick vicariously, hearing the entrepreneur's rags to riches story…then you came to the right place.

- Even our ideas have ideas. ONLY BANK IN CANADA WITH CG. The solutions within our CG are excellent. We are competitively priced and we guarantee and stand behind our solutions. What a great option for our customers and another great reason that companies choose to deal with us. FREE ADVICE FROM LENDERS TOO. We account managers also take the time to ask great questions and add-value by getting our clients thinking in a different direction. We take the time to demonstrate how to complete a cash flow budget, we introduce them to people in our network. Heck, we even refer them customers.

- GIVE ‘EM WHAT THEY ACTUALLY NEED, NOT WHAT WE WANT TO SELL. Sometimes we are best to say ‘no’ because the last thing they really need is more debt. Sometimes we advise them to get a revolving LOC if it’s what they truly need. Other times they ask for $50K for inventory and after our analysis we offer $250K instead because that’s what the business actually needs. We never assume, we ask a lot of probing, onionizing questions to uncover the real needs. VISIT OFTEN. We recently heard from Drar Balshine owner of Sol Cuisine, a manufacturer of tofu-based mock meats. He told us that while he had the same account manager at RBC since he started eight years ago, the guy has only visited the factory once. By contrast, BDC has authorized 4 loans in the last 3 years and we have visited him numerous times. In fact, he joked that we are “3, 4 and 5” with him: three years, four loans, and he’s on to his fifth account manager. He said, “you change your account managers a lot but every one of them has been keen to come for a plant tour and learn how my business runs and I really value that.”

- It’s our job to marry ideas to capital. We’re in the SME growing business.

- HIGHER APPETITE FOR RISK: Not operational risk in the weak company sense. Risk in the credit appetite sense. Leverage. For example, we can stomach 80-100% LTVs on construction financings, and 125% on equipment. We have the long amortizations compared to equipment lessors. NOT BOUND BY PRUDENT LENDING RULES. As a Crown we are ‘above the law’ so to speak with our solutions- a great way to sell the Bank. CASHFLOW LENDER. We know that security isn’t what repays loans, it is cashflow. We are not a cookie cutter lender based on security coverage. It’s not that security is unimportant, it’s just that it falls much further down our list while for all other banks it is number one. EVERY LOAN WE HAVE PRESERVES W/C. Who couldn’t use another $250K for inventory. Every growing company needs cash and CG. Growth = change and change = CG. So don’t ask dumb questions like, ‘do you have any expansion financing needs right now?’ You’ll get the same ‘just browsing’ reaction they give clerks at the Bay. You can probe better than that.

- LOW UP-FRONT FEES. Rarely need appraisals nor environmental studies which saves the clients a load of $$$. Imagine the impact on ‘true cost’ when he’s comparing our rate to the chartered banks. Saving $5,000 at time zero in a NPV calculation makes us a lot cheaper in comparison. NO COVENANTS UNDER $1M. Rarely use D/E and W/C covenants, nor assignments of shareholder loans.

- No monthly margining reports, no annual renewal decisions, no quarterly financial statements.

- PEOPLE LOVE TO HATE THE BANKS. The Credit Unions in Western Canada make hay by simply stating ‘we’re not a bank.’ We can do the same.

- DON’T GET TOO PERSONAL: We ask for limited Personal Guarantees Our guarantees are non-collateralized And are NEVER supported with a charge on residential property (chartered banks prefer SMEs pledge their homes) We won’t finance non-business assets and we won’t collateralize them either…. …So you could say we are the only pure commercial lender in the country. SAD WILL TAKE ACTION. Again, never tell a client we won’t act on our guarantees. SAD will act. If necessary they’ll obtain a Writ of Execution which acts like a 2nd mortgage on title to their home if they still have one. Completely different than pledging the home at the outset though. It only effects their ability to sell their home later.

- HUGE selling feature!

- EASY TO GET ALONG WITH. We’re not in your face every month asking for reports and collecting fees for every little request. Instead, we’ll take you out to lunch once a year to celebrate your success.

- WE MAKE IT EASY. Privileged postponements, top-up loans, unsolicited rate concessions, sunset clauses, SARS loans, seasonal payments, etc.. Client surveys tell us again and again that they appreciate this flexibility. “WHO IS THIS…?” We get such pleasure from calling people up unexpectedly and dropping their interest rate. WE HELP THE SMALL GUYS. We have a mandate to support both start-ups and small loans <$250K. Our appetite doesn’t fluctuate. START-UPS COST US MONEY. Like every other bank on the planet we cannot make money doing it. But unlike every bank we ALWAYS will (due entirely to who our shareholder is – it’s our raison d’etre)

- We have a huge appetite for risk. Particularly on leverage. We can do some pretty creative lending that others can’t.

- WE’RE HUNGRY FOR BUSINESS. Because every BD has to do 3 loans a month, every month, our clients benefit because we are always keen to lend. We are always ‘open for business.’ Our loan appetite is insatiable. Credit doesn’t turn the taps on & off PORTFOLIO REBALANCING. At BDC, we never get memos coming down from Credit telling us to avoid certain industries or certain loan types. Our portfolio contains one asset: a term loan, so there’s nothing to rebalance. We will never experience Credit saying “our portfolio is over weighted with commercial mortgages so no more approvals.” THEY VALUE THE TRANSACTION NOT THE RELATIONSHIP. How many times have you heard prospects say, “Oh, their hospitality portfolio is full so we were referred to the BDC.” What kind of business partner can this be? The BDC is not sector sensitive. If the business is eligible for financing then we would be happy to explore opportunities. WE HAVE FAVOURITES. What are they? Auto, plastics, food, fabricated metals. They borrow more, more often.

- DON’T JUST TAKE OUR WORD FOR IT. Our clients consistently tell us they are very satisfied. Other banks simply cannot make that claim.

- In summary, we are nice complement to their regular daily bank.

- ANTICIPATE. Objections at BDC can be anticipated because you will get the same ones over and over. You can therefore be well practised and prepared. QUESTION: So what is the most common objection most of us hear from our prospects and our influencers? “You are more expensive!”

- NEVER FAX AN OFFER. You need to be there to fully explain, to ‘gauge’ the body language, to see the light of comprehension in their eyes, and the sound of assent in their voice …and you may just need to overcome an objection

- ACKNOWLEDGE THE OBJECTION. If a client claims our rates are too high, acknowledge the feeling first and then turn it around. Avoid the temptation to say bluntly to the client, “You’re wrong,” or, “Actually, no they’re not,” “…you’re not listening, let me explain it to you again!” Nothing good comes from putting the client on the defensive. Try, “I hear what you’re saying, it can certainly appear like that at first, but this spreadsheet may show that…” and deliver your turnaround (see upcoming slides).

- Your interest is too high is a common response. Sometimes our rates are higher, sometimes not. If higher, then you want to emphasize the benefits discussed earlier (non-demand, no charge on your house, etc.) BIG PICTURE…is that we are not trying to compete on interest rate. We are just trying to help them feel they are not overpaying.

- …THEY ARE HARD TO PICK UP. Be careful about promising a low rate too early. So much harder to take it back later. Say things like, “rate could be up to 10%”

- This tool demonstrates to clients what their true rate is so they compare effectively apples to apples. The aim is to demonstrate that the difference isn’t as great as they thought.

- STICKER SHOCK. Flipchart something along the lines of “If I give you $250,000 to buy inventory, you flip that inventory 7 times a year at a 35% gross margin you’ll create $612,500 dollars of incremental contribution that wouldn’t have been possible without my loan. Even at 12% interest the rate is a teeny, teeny fraction ($30K in fact) of how much you’ll make off the inventory, and that’s just in one year, let alone repeating it yearly. I really oughta charge ya 20% - ha!” SUPPLIER DISCOUNT. Add in the fact that you get 3%/10 net 30 discount and the loan has just paid for itself. CHUNK DOWN PRINCIPAL. With us you build equity in the asset quickly and can then borrow against it again really soon. BETTER CASHFLOW. For the first 18 months or a blended payment will be less than our straight-lined principal + interest. But then it crosses over and for the remainin 13.5 years of the amortization, we’re the lower cashflow option.

- COFFEE MATH. Essentially when you look at BDC at 7% and the Chartered Bank and 6.5% it may seem like a giant difference but monetize the difference and break it down to a daily cost. For example, on a $240,000 loan it amounts to $1,200 a year or $3.28 a day which is about the same as a Starbuck’s mocha latte. When you factor in the non-demand benefit, the lower personal guarantee, the lower annual fees, the no appraisal savings and so on it doesn’t add up to a whole lot.

- HAVE THEY SUFFERED BEFORE? Probe to see if they’d had a negative experience with another bank before on a guarantee. Is this a deal-breaker or not? NOT ON YOUR HOUSE. Emphasize the non-collateralized aspect of ours. MISERY LOVES COMPANY. 24,500 other customers have given us one. S.A.D. IS FRIENDLY. We have a (relatively) friendly SAD department. TEST OF COMMITMENT…The ol’ ‘put your money where you mouth is’ argument. GET PROOF. Some claim their other Bank doesn’t ask for one. Get a copy of the lending agreement to verify. Often they don’t realize that they have.

- OTHER BANKS CHARGE IT TOO. If not, they’ll get their pound of flesh buried in some other fee. Besides, it’s earnest money. A portion can be refunded after first disbursement. Interest covers the rental of money. Study fees cover the costs of due diligence. Future loans may enjoy a lesser rate. It’s commensurate with the complexity of the deal. Simple loans 0.5%, multiple company multiple year-end construction loans 1.5% (e.g.) COST OF BUSINESS. It simply costs money to originate a deal. Obviously it cannot be done for free, you wouldn’t run your business at a loss either would you? We could as an alternative bury the cost inside the interest rate but then those who got loans would be subsidizing those who did not and that’s not fair. Neither is charging the fee over the life of the loan (study fee is one shot and it’s over). TAX DEDUCTIBLE. DON’T BE APOLOGETIC.

- [image is of journals and general ledger books] HELP THEM SEE THE VALUE. It doesn’t just help us make a more informed lending decision, it benefits their business: We could possibly lend more money right away. Borrowing again from us or any other bank is much, much easier with Review rather than NTR If they are serious about growing their business fast, they have to get serious about the quality of their financials To upgrade to Review or better yet to Audited means they must upgrade their accounting and MIS systems. Then they can start getting YTD and MTD profit and loss statements and might run the business smarter as a result. If they every one to succeed the business or sell it, it’ll be much easier with better quality track record of statements.