R tools for hierarchical time series

•

20 j'aime•6,549 vues

Talk given at EURO/INFORMS, 1 July 2013

Recommandé

Recommandé

Contenu connexe

Similaire à R tools for hierarchical time series

Similaire à R tools for hierarchical time series (20)

Plus de Rob Hyndman

Plus de Rob Hyndman (18)

Dernier

Dernier (20)

R tools for hierarchical time series

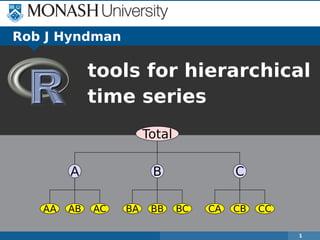

- 1. Total A AA AB AC B BA BB BC C CA CB CC 1 Rob J Hyndman tools for hierarchical time series

- 2. Introduction Total A AA AB AC B BA BB BC C CA CB CC Examples Manufacturing product hierarchies Pharmaceutical sales Net labour turnover hts: R tools for hierarchical time series 2

- 3. Introduction Total A AA AB AC B BA BB BC C CA CB CC Examples Manufacturing product hierarchies Pharmaceutical sales Net labour turnover hts: R tools for hierarchical time series 2

- 4. Introduction Total A AA AB AC B BA BB BC C CA CB CC Examples Manufacturing product hierarchies Pharmaceutical sales Net labour turnover hts: R tools for hierarchical time series 2

- 5. Introduction Total A AA AB AC B BA BB BC C CA CB CC Examples Manufacturing product hierarchies Pharmaceutical sales Net labour turnover hts: R tools for hierarchical time series 2

- 6. Hierarchical/grouped time series A hierarchical time series is a collection of several time series that are linked together in a hierarchical structure. Example: Pharmaceutical products are organized in a hierarchy under the Anatomical Therapeutic Chemical (ATC) Classification System. A grouped time series is a collection of time series that are aggregated in a number of non-hierarchical ways. Example: daily numbers of calls to HP call centres are grouped by product type and location of call centre. hts: R tools for hierarchical time series 3

- 7. Hierarchical/grouped time series A hierarchical time series is a collection of several time series that are linked together in a hierarchical structure. Example: Pharmaceutical products are organized in a hierarchy under the Anatomical Therapeutic Chemical (ATC) Classification System. A grouped time series is a collection of time series that are aggregated in a number of non-hierarchical ways. Example: daily numbers of calls to HP call centres are grouped by product type and location of call centre. hts: R tools for hierarchical time series 3

- 8. Hierarchical/grouped time series A hierarchical time series is a collection of several time series that are linked together in a hierarchical structure. Example: Pharmaceutical products are organized in a hierarchy under the Anatomical Therapeutic Chemical (ATC) Classification System. A grouped time series is a collection of time series that are aggregated in a number of non-hierarchical ways. Example: daily numbers of calls to HP call centres are grouped by product type and location of call centre. hts: R tools for hierarchical time series 3

- 9. Hierarchical/grouped time series A hierarchical time series is a collection of several time series that are linked together in a hierarchical structure. Example: Pharmaceutical products are organized in a hierarchy under the Anatomical Therapeutic Chemical (ATC) Classification System. A grouped time series is a collection of time series that are aggregated in a number of non-hierarchical ways. Example: daily numbers of calls to HP call centres are grouped by product type and location of call centre. hts: R tools for hierarchical time series 3

- 10. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 11. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 12. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 13. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 14. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 15. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 16. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 17. Hierarchical/grouped time series Forecasts should be “aggregate consistent”, unbiased, minimum variance. Existing methods: ¢ Bottom-up ¢ Top-down ¢ Middle-out How to compute forecast intervals? Most research is concerned about relative performance of existing methods. There is no research on how to deal with forecasting grouped time series. hts: R tools for hierarchical time series 4

- 18. Hierarchical data Total A B C hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 19. Hierarchical data Total A B C hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 20. Hierarchical data Total A B C Yt = [Yt, YA,t, YB,t, YC,t] = 1 1 1 1 0 0 0 1 0 0 0 1 YA,t YB,t YC,t hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 21. Hierarchical data Total A B C Yt = [Yt, YA,t, YB,t, YC,t] = 1 1 1 1 0 0 0 1 0 0 0 1 S YA,t YB,t YC,t hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 22. Hierarchical data Total A B C Yt = [Yt, YA,t, YB,t, YC,t] = 1 1 1 1 0 0 0 1 0 0 0 1 S YA,t YB,t YC,t Bt hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 23. Hierarchical data Total A B C Yt = [Yt, YA,t, YB,t, YC,t] = 1 1 1 1 0 0 0 1 0 0 0 1 S YA,t YB,t YC,t Bt Yt = SBt hts: R tools for hierarchical time series 5 Yt : observed aggregate of all series at time t. YX,t : observation on series X at time t. Bt : vector of all series at bottom level in time t.

- 24. Hierarchical data Total A AX AY AZ B BX BY BZ C CX CY CZ Yt = Yt YA,t YB,t YC,t YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t = 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 S YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t Bt hts: R tools for hierarchical time series 6

- 25. Hierarchical data Total A AX AY AZ B BX BY BZ C CX CY CZ Yt = Yt YA,t YB,t YC,t YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t = 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 S YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t Bt hts: R tools for hierarchical time series 6

- 26. Hierarchical data Total A AX AY AZ B BX BY BZ C CX CY CZ Yt = Yt YA,t YB,t YC,t YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t = 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 S YAX,t YAY,t YAZ,t YBX,t YBY,t YBZ,t YCX,t YCY,t YCZ,t Bt hts: R tools for hierarchical time series 6 Yt = SBt

- 27. Grouped data Total A AX AY B BX BY Total X AX BX Y AY BY Yt = Yt YA,t YB,t YX,t YY,t YAX,t YAY,t YBX,t YBY,t = 1 1 1 1 1 1 0 0 0 0 1 1 1 0 1 0 0 1 0 1 1 0 0 0 0 1 0 0 0 0 1 0 0 0 0 1 S YAX,t YAY,t YBX,t YBY,t Bt hts: R tools for hierarchical time series 7

- 28. Grouped data Total A AX AY B BX BY Total X AX BX Y AY BY Yt = Yt YA,t YB,t YX,t YY,t YAX,t YAY,t YBX,t YBY,t = 1 1 1 1 1 1 0 0 0 0 1 1 1 0 1 0 0 1 0 1 1 0 0 0 0 1 0 0 0 0 1 0 0 0 0 1 S YAX,t YAY,t YBX,t YBY,t Bt hts: R tools for hierarchical time series 7

- 29. Grouped data Total A AX AY B BX BY Total X AX BX Y AY BY Yt = Yt YA,t YB,t YX,t YY,t YAX,t YAY,t YBX,t YBY,t = 1 1 1 1 1 1 0 0 0 0 1 1 1 0 1 0 0 1 0 1 1 0 0 0 0 1 0 0 0 0 1 0 0 0 0 1 S YAX,t YAY,t YBX,t YBY,t Bt hts: R tools for hierarchical time series 7 Yt = SBt

- 30. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 31. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 32. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 33. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 34. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 35. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 36. Forecasts Key idea: forecast reconciliation ¯ Ignore structural constraints and forecast every series of interest independently. ¯ Adjust forecasts to impose constraints. Let ˆYn(h) be vector of initial h-step forecasts, made at time n, stacked in same order as Yt. Yt = SBt . So ˆYn(h) = Sβn(h) + εh . βn(h) = E[Bn+h | Y1, . . . , Yn]. εh has zero mean and covariance Σh. Estimate βn(h) using GLS? hts: R tools for hierarchical time series 8

- 37. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 38. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 39. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 40. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 41. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 42. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 43. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 44. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 45. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 46. Optimal combination forecasts ˜Yn(h) = S ˆβn(h) = S(S Σ† hS)−1 S Σ† h ˆYn(h) Revised forecasts Initial forecasts Σ† h is generalized inverse of Σh. Problem: Σh hard to estimate. Solution: Assume εh ≈ SεK,h where εK,h is the forecast error at bottom level. Then Σh ≈ SΩhS where Ωh = Var(εK,h). If Moore-Penrose generalized inverse used, then (S Σ† S)−1 S Σ† = (S S)−1 S . ˜Yn(h) = S(S S)−1 S ˆYn(h) hts: R tools for hierarchical time series 9

- 47. Optimal combination forecasts ˜Yn(h) = S(S S)−1 S ˆYn(h) GLS = OLS. Optimal weighted average of initial forecasts. Optimal reconciliation weights are S(S S)−1 S . Weights are independent of the data and of the covariance structure of the hierarchy! hts: R tools for hierarchical time series 10

- 48. Optimal combination forecasts ˜Yn(h) = S(S S)−1 S ˆYn(h) GLS = OLS. Optimal weighted average of initial forecasts. Optimal reconciliation weights are S(S S)−1 S . Weights are independent of the data and of the covariance structure of the hierarchy! hts: R tools for hierarchical time series 10

- 49. Optimal combination forecasts ˜Yn(h) = S(S S)−1 S ˆYn(h) GLS = OLS. Optimal weighted average of initial forecasts. Optimal reconciliation weights are S(S S)−1 S . Weights are independent of the data and of the covariance structure of the hierarchy! hts: R tools for hierarchical time series 10

- 50. Optimal combination forecasts ˜Yn(h) = S(S S)−1 S ˆYn(h) GLS = OLS. Optimal weighted average of initial forecasts. Optimal reconciliation weights are S(S S)−1 S . Weights are independent of the data and of the covariance structure of the hierarchy! hts: R tools for hierarchical time series 10

- 51. Optimal combination forecasts Total A AA AB AC B BA BB BC C CA CB CC Weights: S(S S)−1 S = 0.69 0.23 0.23 0.23 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.23 0.58 −0.17 −0.17 0.19 0.19 0.19 −0.06 −0.06 −0.06 −0.06 −0.06 −0.06 0.23 −0.17 0.58 −0.17 −0.06 −0.06 −0.06 0.19 0.19 0.19 −0.06 −0.06 −0.06 0.23 −0.17 −0.17 0.58 −0.06 −0.06 −0.06 −0.06 −0.06 −0.06 0.19 0.19 0.19 0.08 0.19 −0.06 −0.06 0.73 −0.27 −0.27 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 0.19 −0.06 −0.06 −0.27 0.73 −0.27 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 0.19 −0.06 −0.06 −0.27 −0.27 0.73 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 0.73 −0.27 −0.27 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 −0.27 0.73 −0.27 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 −0.27 −0.27 0.73 −0.02 −0.02 −0.02 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.73 −0.27 −0.27 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 −0.27 0.73 −0.27 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 −0.27 −0.27 0.73 hts: R tools for hierarchical time series 11

- 52. Optimal combination forecasts Total A AA AB AC B BA BB BC C CA CB CC Weights: S(S S)−1 S = 0.69 0.23 0.23 0.23 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.08 0.23 0.58 −0.17 −0.17 0.19 0.19 0.19 −0.06 −0.06 −0.06 −0.06 −0.06 −0.06 0.23 −0.17 0.58 −0.17 −0.06 −0.06 −0.06 0.19 0.19 0.19 −0.06 −0.06 −0.06 0.23 −0.17 −0.17 0.58 −0.06 −0.06 −0.06 −0.06 −0.06 −0.06 0.19 0.19 0.19 0.08 0.19 −0.06 −0.06 0.73 −0.27 −0.27 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 0.19 −0.06 −0.06 −0.27 0.73 −0.27 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 0.19 −0.06 −0.06 −0.27 −0.27 0.73 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 0.73 −0.27 −0.27 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 −0.27 0.73 −0.27 −0.02 −0.02 −0.02 0.08 −0.06 0.19 −0.06 −0.02 −0.02 −0.02 −0.27 −0.27 0.73 −0.02 −0.02 −0.02 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 0.73 −0.27 −0.27 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 −0.27 0.73 −0.27 0.08 −0.06 −0.06 0.19 −0.02 −0.02 −0.02 −0.02 −0.02 −0.02 −0.27 −0.27 0.73 hts: R tools for hierarchical time series 11

- 53. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 54. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 55. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 56. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 57. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 58. Features Forget “bottom up” or “top down”. This approach combines all forecasts optimally. Method outperforms bottom-up and top-down, especially for middle levels. Covariates can be included in initial forecasts. Adjustments can be made to initial forecasts at any level. Very simple and flexible method. Can work with any hierarchical or grouped time series. Conceptually easy to implement: OLS on base forecasts. hts: R tools for hierarchical time series 12

- 59. Challenges Computational difficulties in big hierarchies due to size of the S matrix and non-singular behavior of (S S). Need to estimate covariance matrix to produce prediction intervals. hts: R tools for hierarchical time series 13

- 60. Challenges Computational difficulties in big hierarchies due to size of the S matrix and non-singular behavior of (S S). Need to estimate covariance matrix to produce prediction intervals. hts: R tools for hierarchical time series 13

- 61. hts package for R hts: R tools for hierarchical time series 14 hts: Hierarchical and grouped time series Methods for analysing and forecasting hierarchical and grouped time series Version: 3.01 Depends: forecast Imports: SparseM Published: 2013-05-07 Author: Rob J Hyndman, Roman A Ahmed, and Han Lin Shang Maintainer: Rob J Hyndman <Rob.Hyndman at monash.edu> License: GPL-2 | GPL-3 [expanded from: GPL (≥ 2)]

- 62. Example using R library(hts) # bts is a matrix containing the bottom level time series # g describes the grouping/hierarchical structure y <- hts(bts, g=c(1,1,2,2)) hts: R tools for hierarchical time series 15

- 63. Example using R library(hts) # bts is a matrix containing the bottom level time series # g describes the grouping/hierarchical structure y <- hts(bts, g=c(1,1,2,2)) hts: R tools for hierarchical time series 15 Total A AX AY B BX BY

- 64. Example using R library(hts) # bts is a matrix containing the bottom level time series # g describes the grouping/hierarchical structure y <- hts(bts, g=c(1,1,2,2)) # Forecast 10-step-ahead using optimal combination method # ETS used for each series by default fc <- forecast(y, h=10) hts: R tools for hierarchical time series 16

- 65. Example using R library(hts) # bts is a matrix containing the bottom level time series # g describes the grouping/hierarchical structure y <- hts(bts, g=c(1,1,2,2)) # Forecast 10-step-ahead using optimal combination method # ETS used for each series by default fc <- forecast(y, h=10) # Select your own methods ally <- allts(y) allf <- matrix(, nrow=10, ncol=ncol(ally)) for(i in 1:ncol(ally)) allf[,i] <- mymethod(ally[,i], h=10) allf <- ts(allf, start=2004) # Reconcile forecasts so they add up fc2 <- combinef(allf, Smatrix(y)) hts: R tools for hierarchical time series 17

- 66. hts function Usage hts(y, g) gts(y, g, hierarchical=FALSE) Arguments y Multivariate time series containing the bot- tom level series g Group matrix indicating the group structure, with one column for each series when com- pletely disaggregated, and one row for each grouping of the time series. hierarchical Indicates if the grouping matrix should be treated as hierarchical. Details hts is simply a wrapper for gts(y,g,TRUE). Both return an object of class gts. hts: R tools for hierarchical time series 18

- 67. forecast.gts function Usage forecast(object, h, method = c("comb", "bu", "mo", "tdgsf", "tdgsa", "tdfp", "all"), fmethod = c("ets", "rw", "arima"), level, positive = FALSE, xreg = NULL, newxreg = NULL, ...) Arguments object Hierarchical time series object of class gts. h Forecast horizon method Method for distributing forecasts within the hierarchy. fmethod Forecasting method to use level Level used for "middle-out" method (when method="mo") positive If TRUE, forecasts are forced to be strictly positive xreg When fmethod = "arima", a vector or matrix of external re- gressors, which must have the same number of rows as the original univariate time series newxreg When fmethod = "arima", a vector or matrix of external re- gressors, which must have the same number of rows as the original univariate time series ... Other arguments passing to ets or auto.arima hts: R tools for hierarchical time series 19

- 68. Utility functions allts(y) Returns all series in the hierarchy Smatrix(y) Returns the summing matrix combinef(f) Combines initial forecasts optimally. hts: R tools for hierarchical time series 20

- 69. More information hts: R tools for hierarchical time series 21 Vignette on CRAN

- 70. References RJ Hyndman, RA Ahmed, G Athanasopoulos, and HL Shang (2011). “Optimal combination forecasts for hierarchical time series”. Computational Statistics and Data Analysis 55(9), 2579–2589 RJ Hyndman, RA Ahmed, and HL Shang (2013). hts: Hierarchical time series. cran.r-project.org/package=hts. RJ Hyndman and G Athanasopoulos (2013). Forecasting: principles and practice. OTexts. OTexts.com/fpp/. hts: R tools for hierarchical time series 22