Mass Affluent Infographic - European Comparison

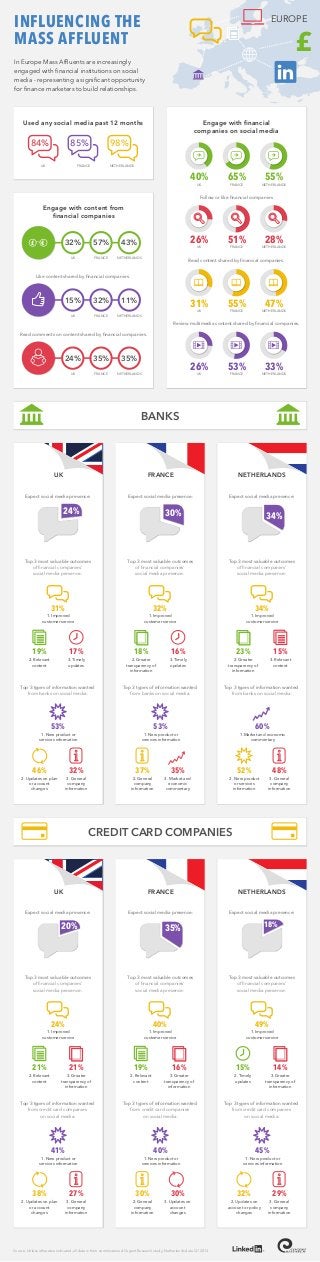

Europeans with significant investable assets expect to engage with finance brands through social media – both to improve their customer experience and to guide future decisions on products and investments. The Mass Affluent, those with investable assets of between €75,000 and €750,000, are amongst the most active and engaged social media users – and see social platforms as an essential element in their relationships with financial institutions. In a groundbreaking study by LinkedIn and Cogent covering France, The Netherlands and the UK, more than 84% of the mass affluent audience in each country were active on social platforms; at least 40% engaged with financial companies, and at least 30% read content shared by those companies. In each country, mass affluent audiences opted for LinkedIn as their most trusted social media source for financial information, and the platform they are most likely to turn to for the content that matters to them. Information on new products and services, market commentary, service updates and general company information figured prominently amongst the most sought-after content from banks, credit card companies, insurance brands and brokers. When asked what they hoped to gain from engaging with such companies through social media, Mass Affluents pointed to improved customer service, greater transparency and timely, relevant content. Across all three countries, and all types of financial sectors, the information discovered and considered through social media is a key driver of immediate action amongst the mass affluent audience. Of those using social media for both discovery and consideration, 63% were driven to take action such as purchasing a product or opening an account. And the comments that Mass Affluents share have a vital role to play in amplifying awareness and engagement amongst their peers. Almost a quarter of those in the UK and over a third of those in France and The Netherlands read others comments on the content shared by financial companies.

Recommended

Recommended

More Related Content

More from LinkedIn Europe

More from LinkedIn Europe (20)

Mass Affluent Infographic - European Comparison

- 1. Source: Unless otherwise indicated, all data is from commissioned Cogent Research study, Netherlands data Q1 2013 INFLUENCING THE MASS AFFLUENT In Europe Mass Affluents are increasingly engaged with financial institutions on social media - representing a significant opportunity for finance marketers to build relationships. 1. Improved customer service 3. Timely updates 2. Relevant content £ Used any social media past 12 months 84% 85% 98% Engage with content from financial companies Engage with financial companies on social media UK 26% FRANCE 51% NETHERLANDS 28% Follow or like financial companies UK 31% FRANCE 55% NETHERLANDS 47% Read content shared by financial companies. UK FRANCE NETHERLANDS Expect social media presence: Expect social media presence: Expect social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: UK UK BANKS FRANCE NETHERLANDS 15% 32% 11% Like content shared by financial companies. Read comments on content shared by financial companies. UK FRANCE NETHERLANDS 24% 35% 35% UK 26% FRANCE 53% NETHERLANDS 33% Review multimedia content shared by financial companies. UK 40% FRANCE 65% NETHERLANDS 55% UK FRANCE NETHERLANDS 32% 57% 43%£ € FRANCE NETHERLANDS 20% 35% 18% 31% 19% 3. Relevant content 15%17% 1. Improved customer service 3. Timely updates 2. Greater transparency of information 32% 18% 16% 1. Improved customer service 2. Greater transparency of information 34% 23% 1. New product or services information 3. General company information 2. Updates on plan or account changes Top 3 types of information wanted from banks on social media: Top 3 types of information wanted from banks on social media: Top 3 types of information wanted from banks on social media: 53% 46% 32% 1. New product or services information 3. Market and economic commentary 53% 35% 2. General company information 37% 1.Market and economic commentary 3. General company information 60% 2. New product or services information 52% 48% 1. Improved customer service 3. Greater transparency of information 2. Relevant content Expect social media presence: Expect social media presence: Expect social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: Top 3 most valuable outcomes of financial companies’ social media presence: UK CREDIT CARD COMPANIES FRANCE NETHERLANDS 24%24% 30% 34% 24% 21% 2. Relevant content 19%21% 2. Timely updates 15% 1. Improved customer service 40% 1. Improved customer service 49% 3. Greater transparency of information 16% 3. Greater transparency of information 14% 1. New product or services information 3. General company information 2. Updates on plan or account changes Top 3 types of information wanted from credit card companies on social media: Top 3 types of information wanted from credit card companies on social media: Top 3 types of information wanted from credit card companies on social media: 41% 38% 27% 1. New product or services information 3. Updates on account changes 40% 30% 2. Updates on account or policy changes 32% 1. New product or services information 45% 2. General company information 30% 3. General company information 29% EUROPE