2011 Training Industry Report

•

3 j'aime•2,978 vues

2011 Training industry report and sizing. Great overview of the corporate training market.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Dernier

Dernier (20)

2011 Training Industry Report

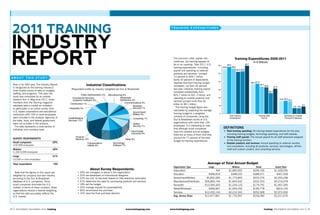

- 1. 2O11 TRAINING TRAINING EXPENDITURES INDUSTRY REPORT The economic roller coaster ride continues, but training appears to be on an upswing: Total 2011 U.S. training expenditures—including payroll and spending on external products and services—jumped 60 50 55.8 58.5 Training Expenditures 2006-2011 56.2 52.2 52.8 59.7 In $ Billions ABOUT THIS STUDY 13 percent to $59.7 billion. Some 32 percent of respondents 40 reported that their training budget 36.3 37.5 Now in its 30th year, The Industry Report 10. Industrial Classifications purchases Who controls traditional training increased—up from 24 percent 33.7 32.9 31.3 is recognized as the training industry’s Respondent profile by industry (weighted per Dun & Bradstreet). last year. Likewise, training payroll 30 most trusted source of data on budgets, 25.7 increased substantially, from staffing, and programs. This year, the Public Administration 2% Manufacturing 9% $25.7 billion to $31.3 billion, and study was conducted by an outside Wholesale/ Educational Services/ spending on outside products and 20 research firm in May/June 2011, when Academic Institution 8% Distribution 3% 15.8 16.3 15.4 services jumped more than $2 members from the Training magazine Construction 1% Communications 3% billion to $9.1 billion. 9.1 database were e-mailed an invitation Business 10 7.0 6.9 Hospitality 3% Services 7% The training budget figure was to participate in an online survey. Only U.S.-based corporations and educational calculated by projecting the average Government/ institutions with 100 or more employees Military 6% training budget to a weighted 0 universe of companies, using the Total Training Training Staff Spending on Outside were included in the analysis. Agencies of Health/Medical Consulting 1% Expenditures Payroll Products & Services the state, local, and federal government Services 17% Dun & Bradstreet counts of U.S. were not included in the analysis. Safety/ organizations with more than 100 The data represents a cross-section of Security 1% employees. It is interesting to note that although small companies DEFINITIONS industries and company sizes. Real Estate/ have the smallest annual budgets, Total training spending: All training-related expenditures for the year, Insurance 9% including training budgets, technology spending, and staff salaries. there are so many of them that they Finance/ account for 77 percent of the total Training staff payroll: The annual payroll for all staff personnel assigned Survey Respondents Banking 14% Retail 3% 02. training budget breakdowns budget for training expenditures. to the training function. Small companies 29% Transportation/ Technology/ Outside products and services: Annual spending on external vendors (100-999 employees) Utilities 6% Software 7% and consultants, including all products, services, technologies, off-the- Midsize 40% shelf and custom content, and consulting services. (1,000-9,999 employees) Large 31% (10,000 or more employees) Total respondents 790 Average of Total Annual Budget Organization Type Large Midsize Small Grand Total About Survey Respondents: Association N/A $1,800,000 $256,100 $1,028,050 Note that the figures in this report are • 49% are managers or above in the organization • 25% are developers or instructional designers Education $996,818 $398,533 $388,571 $467,538 weighted by company size and industry according to the Dun & Bradstreet • 22% are mid- to low-level (based on title selection) associates Government/Military $5,852,000 $1,775,800 $225,276 $2,000,298 database of U.S. companies. Since • 51% determine the need for purchasing products and services Manufacturer/Distributor $28,860,744 $1,843,542 $332,333 $5,216,078 small companies dominate the U.S. • 18% set the budget Nonprofit $12,093,320 $1,234,125 $179,791 $1,957,395 market, in terms of sheer numbers, these • 26% manage request for proposals/bids Retail/Wholesale 51.1 $466,667 55.8 58.5 $1,656,250 56.2 52.2 $185,778 52.2 $816,100 organizations receive a heavier weighting, • 66% recommend the purchase 37.5 36.3 37.5 33.7 32.9 32.8 $3,974,934 • 16% have the final purchase decision Services $12,403,144 $2,212,342 $252,928 so that the data accurately reflects the U.S. market. Avg. Across Sizes 13.5 $12,677,841 15.8 16.3 $1,776,997 15.4 7.0 $256,082 7.0 $3,221,676 22 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 23

- 2. 2011 Training Industry Report TRAINING EXPENDITURES Types of Training Products and Services Training Expenditures per Learner 2009-2011 Intended to Purchase Next Year $1,036 n 2009 Assessment & Analysis Testing 23% All Companies $1,041 n 2010 $749 n 2011 Audience Response Systems 7% Audio and Web Conferencing Products & Systems 24% $1,176 Small (10 to 999 $1,076 Authoring Tools/Systems 32% employees) $922 Business Skills 16% Certification 24% $975 Midsize (1,000 to $702 Classroom Tools & Systems 32% 9,999 employees) $761 Consulting 25% Content Development 30% Large (10,000 or $886 Courseware Design 21% $671 more employees) $375 Customer Relationship Management 9% 0 200 400 600 800 1000 1200 Enterprise Learning Systems 8% Games & Simulations 22% Knowledge Management Tools/Systems 17% Hours of Training per Employee 2010-2011 Learning Management Systems 30% 40.1 Mobile Learning 20% All Companies 39.3 n 2010 Online Learning Tools & Systems 38% n 2011 Small (10 to 999 40.9 Support/On-Demand Learning Tools & Systems 13% employees) 36.6 Presentation Software & Tools 25% Midsize (1,000 to 40.6 Talent Management Tools & Systems 14% 37.3 9,999 employees) Training Management Administration 10% Large (10,000 or 36.7 Translation & Localization 10% 49.5 more employees) Web 2.0 6% 0 10 20 30 40 50 0 5 10 15 20 25 30 35 40 The contribution of large companies decreased, although and technologies. Looking ahead, nearly 40 percent of $2 million. Across all organization types, larger companies On average, employees receive 39 hours of training per the number of large companies increased this year. Midsize organizations plan to purchase online learning tools and spend roughly five times as much as midsize ones, and year, one hour less than last year. While large retail/wholesale companies showed the greatest increase compared to last systems in the coming year, while approximately 30 percent midsize companies spend approximately five times as organizations have the highest average number of hours year, going from $8.89 billion to $12.47 billion. Both the said they would buy authoring tools/systems, classroom tools much as small ones. The average payroll figure for large overall (93), government/military organizations have the number of midsize companies and the base budget for and systems, and learning management systems. These companies was $3.8 million; for midsize organizations, it greatest number of hours regardless of size (average of 68). them increased this year. Small companies had a modest (9 numbers are virtually the same as last year. Intent to purchase was $745,663; for small companies, it was $142,294. The Executives saw a decline in their share of training resources, percent) increase in the average total budget, but the number audio and Web conferencing products and systems declined overall average for all companies was $1 million. from 22 percent of the training spend down to 10 percent in of small companies decreased by 10 percent. The total from 27 percent in 2010 to 24 percent in 2011. Overall, on average, companies spent $749 per learner this 2011. Non-exempt employees saw their share rebound back contribution by small companies increased 7 percent this year. The jump in payroll can be attributed in part to a significant year compared with $1,041 per learner in 2010. Increased to 2009 levels at 41 percent, up from 26 percent in 2010. Other expenditures decreased slightly to $19.3 billion from increase in training staff. Some 29 percent of organizations staffing, economies of scale, and costs saved by moving to Like last year, the highest percentage of organizations (26 $20.1 billion in 2010. On average, organizations spent 19 said they increased staff from the year before (up from 16 e-learning factor into the decreased spend per learner. percent) said management/supervisory training will receive percent of their budget or $345,791 on learning tools and percent in 2010), while 55 percent said the level remained For those who reported an increase in their training staff, more funding than last year. On average, organizations plan technologies. Manufacturers/distributors had the largest the same (down from 61 percent in 2010). Only 16 percent the average increase was six people, the same as in 2010. to allocate the most funding to professional/industry-specific budget in this area, while small retail/wholesale organizations said it was lower, vs. 23 percent in 2010. Manufacturers/ For those who reported a decrease in their staff, the average training ($2.7 million), followed by IT/systems training at spent a larger portion of their budgets on learning tools distributors have the largest personnel costs at an average of decrease was nine people—down from 10 last year. $848,327 and mandatory/compliance training ($680,379). 24 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 25

- 3. 2011 Training Industry Report TRAINING EXPENDITURES TRAINING BUDGETS Training Expenditure Allocations— The average training budget for large What Happened to Your Who Gets Trained? companies was $12.7 million (down Training Budget This Year? Staff per 1,000 Learners from $15.9 million in 2010), while 50 41% Midsize Companies midsize companies allocated an 40 average of $1.8 million (up from $1.3 15 million last year), and small companies 30 24% 25% 11.4 12.2 Decreased 12 Increased 9.2 $256,082 (up from $234,850). 25% 20 9 The majority of companies—43 32% 10% 6 percent—said their training budget 10 3 remained the same, while 32 percent 0 0 said it went up and 25 percent said it Remained Executives Managers, Non- Non- Overall 1,000 to 5,000 to the same Exempt Managers, Exempt decreased; this is a reversal from last for Midsize 4,999 9,999 43% Exempt Employees Companies year, when 32 percent said it decreased and 24 percent said it increased. Some 42.9 percent saw increases in Staff per 1,000 Learners Staff per 1,000 Learners the 6 to 15 percent range, while 37.4 Large Companies Small Companies percent reported increases in the 1 to 5 25 24.0 12 11.1 percent range. More midsize companies 10 20 18.8 19.0 reported an increase in budget overall. 8.0 7.9 Most respondents who reported an 8 6.4 15 14.1 increase in their training budgets 6 attributed it to the following reasons: 10 4 Budget Change by Industry 2 5 • Increase in the scope of their training programs (67 percent; up from 57 15% n Decrease 0 0 35% Overall 10,000 to 25,000 to 50,000 or Overall for 100 to 250 to 500 to percent in 2010) Manufacturer/Distributor n Increase for Large 24,999 49,999 more Small 249 499 999 • More learners served (62 percent; up 50% n Same Companies Companies from 43 percent last year) 23% • Added training staff (52 percent; up Services 33% from 33 percent) 44% The average training Is the Number of Training-Related Staff Higher Retail/Wholesale 19% 29% 52% budget for large or Lower Than Last Year? 44% companies was Government/Military 15% 41% Lower $12.7 million, while Higher 29% 16% Education 16% 38% 47% midsize companies 0% allocated an average of Association 100% Same 0% 55% $1.8 million, and small Nonprofit 22% 38% 41% companies dedicated an 0 20 40 60 80 100 average of $256,082. 26 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 27

- 4. 2011 Training Industry Report TRAINING BUDGETS How Much Did Your Training Budget Increase? How Much Did Your Training Budget Decrease? Like last year, the majority (50 percent) All Companies All Companies of respondents reported budget decreases More Than 25% 11% More Than 25% 16.7% between 6 and 15 percent. More than 60 percent chose “other” as the reason for the 16% to 25% 9% 16% to 25% 15.9% decrease, citing “across-the-board budget 6% to 15% 43% 6% to 15% 50.0% cuts,” “decreasing revenues,” and “economic 17.5% 1% to 5% 37% 1% to 5% reasons,” among others. This was followed by: 0 10 20 30 40 50 0 10 20 30 40 50 • Budget adjustments to reflect lower costs (50 percent; up from 39 percent last year) Small Companies Small Companies • Staff reductions (48 percent; up from 35 More Than 25% 19% More Than 25% 23.3% percent) • Attended fewer outside learning events (42 16% to 25% 11% 16% to 25% 16.7% percent; up from 41 percent) 6% to 15% 35% 6% to 15% 46.7% 1% to 5% 35% 1% to 5% 13.3% The most important priorities for training in terms of allocating resources in 2011 0 10 20 30 40 0 10 20 30 40 50 are: increasing the effectiveness of training programs (28 percent, up from Midsize Companies 26 percent last year) and reducing costs/ Midsize Companies improving efficiencies (the same as 2010 More Than 25% 4% More Than 25% 12.0% at 23 percent), followed by measuring the 16% to 25% 6% 18.0% 16% to 25% impact of training programs and increasing 6% to 15% 52% 6% to 15% 56.0% learner usage of training programs (both with 13 percent). Like last year, learning 1% to 5% 38% 1% to 5% 14.0% infrastructure/technology initiatives and 0 10 20 30 40 50 0 10 20 30 40 50 60 obtaining revenue through external training remain the lowest priorities. Large Companies Large Companies More Than 25% 11% More Than 25% 17.4% 16% to 25% 11% 16% to 25% 13.0% 6% to 15% 37% 6% to 15% 45.7% 1% to 5% 40% 1% to 5% 23.9% 0 10 20 30 40 0 10 20 30 40 50 Why Did Your Budget Increase? Added Training Staff 52% Why Did Your Budget Decrease? Increased Number of Learners Served 62% Reduced Training Staff 48% Increased Scope of Training 67% Decreased Number of Learners Served 21% Attended More Outside Learning Events (conferences/seminars) 21% Decreased Scope of Training 24% Increased Outside Trainer/Consultant Investment 23% Attended Fewer Outside Learning Events (conferences/seminars) 42% Purchased New Technologies/Equipment 47% Decreased Outside Trainer/Consultant Investment 27% Budget Adjusted to Reflect Higher Costs 26% Budget Adjusted to Reflect Lower Costs 50% Other 8% Other 62% 0 10 20 30 40 50 60 70 10 20 30 40 50 60 70 0 28 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 29

- 5. 2011 Training Industry Report TRAINING BUDGETS TRAINING DELIVERY Mandatory or compliance training continues to be done than 10 percent of their programs. Projected Funding for Learning Areas Next Year mostly online, with 73 percent of organizations doing at • Learning Management System (LMS) (69 percent, up from Executive Development 13% 52% 9% 26% least some of it online and 18 percent entirely online. Online 67 percent) Management/Supervisory Training training also often is used for desktop application training • Usage of an application simulation tool increased slightly 26% 52% 10% 12% (59 percent, up from 47 percent last year) and IT/systems from 43 percent last year to 46 percent this year. Interpersonal Skills (e.g., communication, teamwork) 17% 58% 12% 13% application training (60 percent, up from 48 percent last IT/Systems Training (e.g., enterprise software) 18% 51% 12% 19% year). Online training is least used for customer service The delivery methods least often used for training remain Desktop Application Training 13% 56% 14% 17% training (36 percent), executive development (39 percent), the same as last year: and interpersonal skills (38 percent). Of the learning Customer Service Training 20% 52% 7% 21% technologies presented, the most often used include: • Podcasting at 21 percent Sales Training 22% 34% 4% 40% • Online Performance Support (EPSS) or knowledge Mandatory or Compliance Training 21% 66% 4% 9% • Virtual classroom/Webcasting/video broadcasting (76 management system at 23 percent Profession/Industry-Specific (engineering, accounting, etc.) 14% 59% 8% 19% percent, up from 71 percent last year). That said, 54 • Learning Content Management System (LCMS) at percent of companies use virtual training methods for less 26 percent 0 20 40 60 80 100 n More Than Last Year n About the Same as Last Year n Less Than Last Year n N/A TRAINING DELIVERY Online Method Use for Types of Training Executive Development 29% 21% 23% 19% 7% 1% Technology remains a force in training but did not show percent last year. significant gains in 2011. In particular, hours of training • 1.3 percent of training hours are delivered via social Management/Supervisory Training 11% 16% 30% 34% 9% 0% delivered via social networking and mobile declined. networking or mobile devices, down from 7.2 percent last Interpersonal Skills (e.g., communication) 12% 27% 28% 25% 7 1% year. IT/Systems Training (e.g., enterprise software) 17% 14% 20% 26% 20% 3% • 41.6 percent of training hours are delivered by a stand- Desktop Application Training 18% 12% 21% 25% 19% 5% and-deliver instructor in a classroom setting; that figure is Small and midsize companies continue to rely on up significantly from the 27.7 percent reported last year instructor-led delivery methods more so than large Customer Service Training 21% 25% 26% 20% 7% 1% and nearly back to the 47 percent reported in 2009. companies: 45 percent vs. 30 percent. Blended learning Sales Training 43% 17% 17% 19% 4% 0% • 24 percent of hours are delivered with blended learning is fairly even across companies of all sizes at roughly 24 8% 10% 15% 17% 32% 18% Mandatory or Compliance Training techniques, up a bit from 21.9 percent last year. percent. Large companies appear to be focusing on online Profession/Industry-Specific (e.g., engineering) 23% 13% 26% 29% 8% 1% • 21.9 percent of hours are delivered via online or or computer-based methods (28 percent vs. 20 percent for computer-based technologies, down slightly from 23.6 small and midsize companies). 0 20 40 60 80 100 n We Don’t Offer This Training n No Online n A Few Online Programs n Some Online n Mostly Online n All Online Training Delivery Methods by Company Size 2011 Small (10 to 999 employees) 22.3% 45.2% 11.2% 20.5% 0.6% 0.2% Types of Training Delivered by Online Training Methods Executive Development 39% Midsize (1,000 to 9,999 employees) 24.1% 44.4% 10.0% 20.1% 0.7% 0.2% 25% Management/Supervisory Training 48% Interpersonal Skills (e.g., communication) 38% Large (10,000 or more employees) 26.6% 29.4% 13.1% 28.4% 2.1% 0.7% IT/Systems Training (e.g., enterprise software) 60% Desktop Application Training 59% 0 20 40 60 80 100 Customer Service Training 36% n Blended Learning (a combination of methods listed below) n Instructor-Led Classroom Only Sales Training 42% n Virtual Classroom/Webcast Only (instructor from remote location) Mandatory or Compliance Training 73% n Online or Computer-Based Methods Only (no instructor) Profession/Industry-Specific (e.g., engineering) 50% n Social Networking Only (wikis, blogs, communities of practice) 10 0 20 30 40 50 60 70 80 n Mobile Only (cell phones, iPods, PDAs) 30 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 31

- 6. 2011 Training Industry Report TRAINING DELIVERY TRAINING OUTSOURCING Learning Technologies Current Usage All Companies Podcasting 21% 74% 5% Online Performance Support or Knowledge Management System 23% 64% 13% Rapid E-Learning Tool (PowerPoint conversion tool) 50% 43% 7% 2011 saw a significant rise in the average expenditure As with 2011, the level of outsourcing is expected to stay Application Simulation Tool 46% 48% 6% for training outsourcing: $606,563, up from $257,871 in relatively steady in 2012—some 79 percent of organizations 2010. An average of 23 percent of the total training budget said they expect to stay the same in the outsourcing area. Virtual Classroom/Webcasting/Video Broadcasting 76% 22% 2% was spent on outsourcing. And the percentage of companies expecting to increase use Learning Content Management System (LCMS) 26% 63% 11% On average, 18 percent of companies completely outsource is almost exactly offset by those organizations expecting to Learning Management System (LMS) 69% 27% 4% LMS operations/hosting (vs. 21 percent last year). LMS decrease outsourcing for the same functions. On balance, administration, however, continues to be mostly handled large companies will outsource less, especially when it 0 20 40 60 80 100 in-house, with only a small amount outsourced. Learner comes to instruction/facilitation and LMS administration. n Use currently n Do not use n Not sure support is largely handled in-house, as well. Midsize companies may outsource more custom content development. Small Companies • Outsourcing learner support decreased a bit, from 21 Both of the two areas with the least outsourcing this year, Podcasting 11% 84% 5% percent in 2010 to 19 percent in 2011, while custom learner support and LMS administration, anticipate slightly 16% 74% 10% content development rose from 40 percent to 47 percent. less outsourcing vs. slightly more, plus an average of 48 Online Performance Support or Knowledge Management System • Instruction/facilitation again is the most often considered percent said they have no intention of outsourcing those Rapid E-Learning Tool (PowerPoint conversion tool) 41% 54% 5% for some degree of outsourcing, up from 44 percent last functions, so those numbers can be expected to dip again Application Simulation Tool 38% 55% 7% year to 47 percent this year). next year. Virtual Classroom/Webcasting/Video Broadcasting 66% 31% 3% Learning Content Management System (LCMS) 16% 71% 13% Learning Management System (LMS) 52% 43% 5% 0 20 40 60 80 100 2011 saw a significant rise in the average expenditure for training outsourcing: $606,563, n Use currently n Do not use n Not sure Midsize Companies Podcasting 22% 25% 76% 67% 2% 8% up from $257,871 in 2010. An average of 23 percent of the total training budget was spent Online Performance Support or Knowledge Management System Rapid E-Learning Tool (PowerPoint conversion tool) 52% 43% 5% on outsourcing. The level of outsourcing is Application Simulation Tool 45% 52% 3% Virtual Classroom/Webcasting/Video Broadcasting 79% 20% 1% Learning Content Management System (LCMS) Learning Management System (LMS) 29% 74% 61% 24% 10% 2% expected to stay relatively steady in 2012. 0 20 40 60 80 100 n Use currently n Do not use n Not sure Large Companies Podcasting 33% 58% 9% Extent of Outsourcing All Companies Online Performance Support or Knowledge Management System 32% 44% 24% Rapid E-Learning Tool (PowerPoint conversion tool) 58% 28% 14% Instruction/Facilitation 49% 47% 4% Application Simulation Tool 59% 31% 10% LMS Administration (registration, upload data) 79% 18% 3% Virtual Classroom/Webcasting/Video Broadcasting 88% 9% 3% LMS Operations/Hosting 60% 22% 18% Learning Content Management System (LCMS) 35% 55% 10% Learner Support 81% 18% 1% Learning Management System (LMS) 85% 10% 5% Custom Content Development 53% 43% 4% 0 20 40 60 80 100 0 20 40 60 80 100 n Use currently n Do not use n Not sure n No Outsourcing n Some Outsourcing n Mostly or Completely Outsourced 32 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 33

- 7. 2011 Training Industry Report TRAINING OUTSOURCING Extent of Outsourcing Small Companies Projected Use of Outsourcing All Companies Instruction/Facilitation 54% 44% 2% Instruction/Facilitation 10% 47% 10% 33% LMS Administration (registration, upload data) 81% 14% 5% LMS Administration (registration, upload data) 4% 41% 5% 50% LMS Operations/Hosting 65% 18% 17% LMS Operations/Hosting 9% 49% 6% 36% Learner Support 84% 16% 0% Learner Support 4% 41% 9% 46% Custom Content Development 67% 28% 5% Custom Content Development 16% 37% 14% 33% 0 20 40 60 80 100 0 20 40 60 80 100 n More Outsourcing n The Same n Less Outsourcing n No Outsourcing n Some Outsourcing n Mostly or Completely Outsourced n We Don’t/Won’t Outsource This Function Midsize Companies Small Companies Instruction/Facilitation 48% 48% 4% Instruction/Facilitation 9% 45% 7% 39% LMS Administration (registration, upload data) 82% 17% 1% LMS Administration (registration, upload data) 3% 41% 2% 54% LMS Operations/Hosting 57% 21% 22% LMS Operations/Hosting 7% 50% 3% 40% Learner Support 86% 14% 0% Learner Support 4% 39% 6% 51% Custom Content Development 51% 47% 2% Custom Content Development 11% 33% 12% 44% 0 20 40 60 80 100 0 20 40 60 80 100 n More Outsourcing n The Same n Less Outsourcing n No Outsourcing n Some Outsourcing n Mostly or Completely Outsourced n We Don’t/Won’t Outsource This Function Large Companies Midsize Companies Instruction/Facilitation 14% 47% 12% 27% Instruction/Facilitation 46% 49% 5% LMS Administration (registration, upload data) 7% 38% 6% 49% LMS Administration (registration, upload data) 72% 24% 4% LMS Operations/Hosting 13% 45% 7% 35% LMS Operations/Hosting 57% 30% 13% Learner Support 4% 39% 10% 47% Learner Support 68% 30% 2% Custom Content Development 22% 36% 14% 28% Custom Content Development 35% 59% 6% 0 20 40 60 80 100 0 20 40 60 80 100 n More Outsourcing n The Same n Less Outsourcing n No Outsourcing n Some Outsourcing n Mostly or Completely Outsourced n We Don’t/Won’t Outsource This Function In 2012, large companies will outsource Instruction/Facilitation 6% 52% Large Companies 12% 30% less, especially when it comes to instruction/ LMS Administration (registration, upload data) 1% 46% 8% 45% facilitation and LMS administration. Midsize LMS Operations/Hosting 5% 55% 8% 32% Learner Support 6% 49% 11% 34% companies may outsource more custom Custom Content Development 16% 43% 19% 22% 0 20 40 60 80 100 content development. n More Outsourcing n The Same n Less Outsourcing n We Don’t/Won’t Outsource This Function 34 | NOVEMBER/DECEMBER 2011 training www.trainingmag.com www.trainingmag.com training NOVEMBER/DECEMBER 2011 | 35